Directors Fees

Where a company director receives income that is classified specifically as Director’s Fees (and not remuneration under a contract of service), this portion of income is subject to PRSI Class S.

Director’s Fees are defined as payments relating solely to:

- attending board meetings,

- carrying out statutory director duties,

- fulfilling obligations not connected to normal employment,

- and not under an employer–employee contract of service.

Because Director’s Fees fall under PRSI Class S, no Employer PRSI is charged on this portion of income.

You should always confirm correct treatment with an accountant/tax adviser or contact Scope Section if unsure whether part of a director’s earnings qualifies as Director’s Fees.

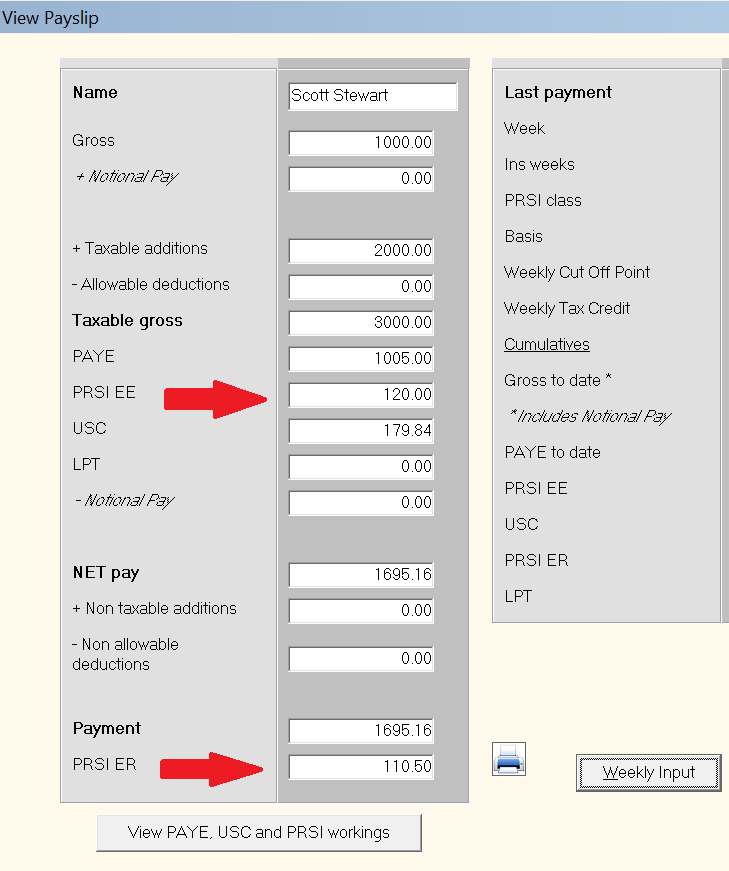

Calculating PRSI with Directors Fees

Employee PRSI (assuming the Director is a Class A contributor)

Director's Weekly Salary/Remuneration €1000.00

Director's Fees €2000.00

Salary/Remuneration (Subject to PRSI Class A1) €1000.00

€1000.00 @ 4.2% (from 1st October 2025) = €42.00

Director's Fees (Subject to PRSI Class S) €2000.00

€2000.00 @ 4.2% (from 1st October 2025) = €84.00

Total Employee PRSI deduction = €126.00

Employer PRSI

Director's Weekly Salary/Remuneration €1000.00

Director's Fees €2000.00

Salary/Remuneration (Subject to PRSI Class A1) €1000.00

€1000.00 @ 11.25% (from 1st October 2025) = €112.50

Director's Fees (Subject to PRSI Class S) €2000.00

No Employer PRSI chargeable under Class S

Total Employee PRSI deduction = €112.50

Revenue submissions will all reflect PRSI contribution for the period at Class A1, as Class A takes precedence over any other PRSI class within a contributory period.

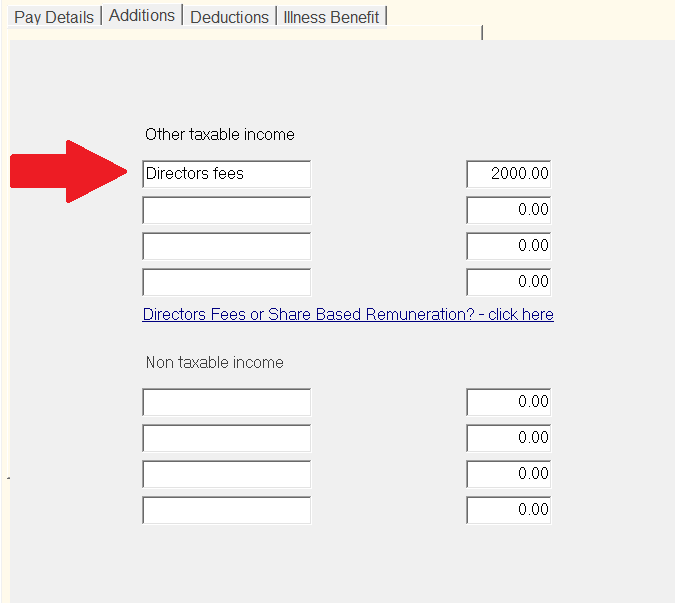

Entering Directors Fees in Thesaurus Payroll Manager

To enter director's fees, go to Process Icon No. 3 or Payslips > Weekly/Monthly/Fortnightly Input

- Select the employee

- Select their "Additions" tab

- Within an available "Other Taxable Income" field, enter "Directors Fees" as the narrative, in order to allocate this field to Directors Fees and to allocate the correct PRSI treatment to any amount entered.

- Once you start to enter "Directors Fees" the field will auto fill.

- The PRSI will be deducted accordingly

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.