Share Based Remuneration

Where an employee is in receipt of Share Based Remuneration, it is subject to PRSI at a flat 4%, regardless of other earnings.

- Share Based Remuneration is subject to Employee PRSI only, it is not subject to Employer PRSI

- Share Based Remuneration should be included as income in determining the appropriate PRSI subclass to apply to the employee's total income, but at all times ensuring that the total portion of Share Based Remuneration is subject to 4%

- Share Based Remuneration should NOT be included as income in determining the appropriate Employer PRSI subclass to apply and in charging Employer PRSI.

- In some cases this may result in a different subclass being applied to the employee and employer PRSI. If this is the case it is always the Employee's subclass that is recorded against the pay period and subsequently returned.

By entering the narrative 'Share based pay' against a taxable additions, the software will split the PRSI calculation accordingly. If the Share based pay is awarded in shares, as opposed to income, then enter a non allowable deduction to the same value.

You may need to confirm this treatment with your accountant/tax advisor or if you are in any doubt as to whether or not any portion of income is to be treated as share based remuneration.

Calculating PRSI with Share Based Remuneration

Employee PRSI

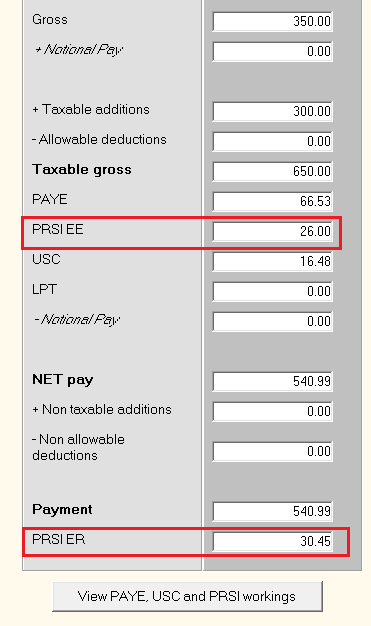

Employees Weekly Salary €350.00

Share Based Remuneration €300.00

Salary/Remuneration (Subject to PRSI Class A1) €350.00

€350.00 @ 4% = €14.00

Share Based Remuneration (Subject to PRSI Class S) €300.00

€300.00 @ 4% = €12.00

Total Employee PRSI deduction €26.00

Employer PRSI

Employees Weekly Salary €350.00

Share Based Remuneration €300.00

Salary/Remuneration (Subject to PRSI Class A)

€350.00 @ 8.70% = €30.45

Share based Remuneration (Subject to PRSI Class S) €300.00

No Employer PRSI chargeable under Class S

Total Employer PRSI deduction €30.45

Revenue submissions will all reflect PRSI contribution for the period at Class A1, as Class A takes precedence over any other PRSI class within a contributory period.

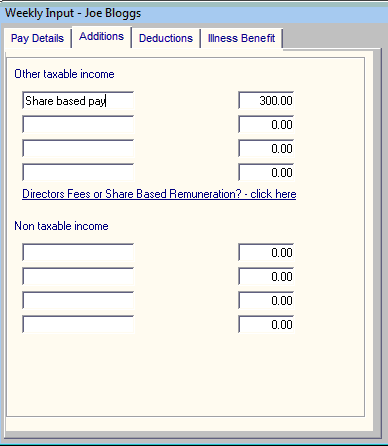

Entering Share Based Remuneration in Thesaurus Payroll Manager

To enter share based remuneration, go to Process Icon No. 3 or Payslips > Weekly/Monthly/Fortnightly Input

- Select the employee

- Select their "Additions" tab

- Within an available "Other Taxable Income" field, enter "Share based pay" as the narrative, in order to allocate this field to Directors Fees and to allocate the correct PRSI treatment to any amount entered.

- Once you start to enter "Share based pay" the field will auto fill.

- The PRSI will be deducted accordingly

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.

Help2019 Thesaurus Payroll Manager - System Requirements2019 Budget - Employer SummaryPayroll CalendarPayroll DeductionsGetting startedImporting from previous yearImporting from other Payroll SoftwareMigrating to Thesaurus Payroll Manager Mid Tax-YearCompany SetupDigital CertificatesAdd/ Amend EmployeesRevenue Payroll Notifications (RPNs)Processing Payroll

Weekly PayrollMonthly PayrollFortnightly PayrollQuick Edit EntryNet to Gross PaymentsPayroll PreviewFinalising the Pay PeriodPayslip WorkingsComputational AnomalySpecifying end dates for additions or deductionsDirectors FeesShare Based RemunerationImporting Hours from Text or CSV FileFull periodic CSV Import

Payroll Submission Requests (PSRs)Distributing PayslipsPaying EmployeesCorrectionsRevenue PaymentsReportsProcessing StartersProcessing LeaversBenefit in KindIllness BenefitMaternity BenefitPaternity BenefitPensionsChanging an Employee's Pay FrequencyYear End - 2019Backup and RestoreCSOHolidaysLeave EntitlementsEmployment LawGeneralGlossary of Terms (Pre 2019)Revenue - Contact Telephone NumbersTransferring Payroll Manager from one PC to anotherThesaurus ConnectGDPREnd User Licence Agreement for Thesaurus Payroll Manager